A GUIDE TO THOUGHTFUL SPENDING

It has never been more tempting to spend money. Every day, we’re pressured to buy something, whether through traditional ads, targeted recommendations or the curated lifestyles of online influencers. The messages are constant and persuasive.

Financial professionals like us spend a lot of time talking about how to save. But knowing how to spend well is equally important. And for many, spending is surprisingly fraught, wrapped up in behavioral biases and the psychological imprints of past experiences.

Unexamined spending can lead to extremes. On one end of the spectrum, you find overspenders who rack up debt and land in financial hot water. On the other end are those afraid to spend, depriving themselves of things they can afford that would give them pleasure.

Ultimately, spending is unavoidable. Ideally, we find a middle path that allows us to cover necessities and spend on the things that truly bring joy, whether that’s hobbies, travel, experiences with your family and friends, or simple everyday pleasures.

So how do you engage in thoughtful spending? These tips can help.

CONSIDER YOUR VALUES

One of the best ways to become a mindful spender is to spend in line with your values. Take the time to identify what matters most to you. These could be things like health, family, community, security or creativity. Before making a purchase, consider whether it supports one or more of these values. Doing so can help you avoid potential behavioral traps, such as signaling—spending money to shape how other people think of us.

It’s one thing to buy a nicer car because you need it. It’s another to buy one because you want to broadcast status to neighbors.

If you can truly afford to do this, there’s not necessarily a lot of harm done financially speaking. But it’s still worth asking whether the motivation reflects something you truly value or simply a desire to impress others.

And if the purchase stretches your finances, the irony is clear: Spending to appear wealthy actually undermines your financial security.

COMPARE AND DESPAIR

Closely related to signaling is the phenomenon of keeping up with the proverbial Joneses.

Morgan Housel, partner at The Collaborative Fund and author of The Psychology of Money puts it well: “There are two ways to use money. One is as a tool to live a better life. The other is as a yardstick of status to measure yourself against others. Many people aspire for the former but get caught up chasing the latter.”

When we see other people spending freely—neighbors renovating their kitchen or friends taking pricey vacations—it can create subtle pressure to match their choices. After all, we humans are deeply wired to avoid appearing like outsiders.

But appearances can be misleading. The people you’re comparing yourself to may be financing those purchases or stretching their budget to maintain a perfect front.

So again, before trying to match anyone’s spending, revisit your own priorities. You may find that the security of living within your means is much more important to you.

BE MINDFUL OF HEDONIC ADAPTATION

Besides being a bit of a mouthful, hedonic adaptation is the tendency for humans to return to a baseline level of happiness even after major positive or negative changes in their lives. In other words, the emotional impact of these events fades quickly over time.

This can have important implications for spending. Many purchases—the latest smartphone, a luxury car, a bigger home—promise lasting happiness. These items might provide a short-term boost in satisfaction, but that feeling typically fades faster than we’d expect.

Understanding this tendency can encourage a bit of pause before making big purchases. If it’s greater happiness you seek, whatever you’re considering buying likely isn’t the solution.

Being mindful of hedonic adaptation can also help guard against lifestyle creep, where spending gradually increases as income rises without necessarily improving long-term happiness. Buying that bigger home requires spending more on things like taxes and upkeep, which may quickly make you feel out of control. Or as Housel puts it: “Sometimes the stuff you spend money on has so much influence over your autonomy…that it’s not clear whether you own things or the things own you.”

On a more reassuring note, just as we adapt to positive changes, we also adapt to setbacks. Difficult events like a job loss or a financial downturn can feel overwhelming in the moment, but emotional recovery tends to be swift.

THINK BEFORE YOU CARPE DIEM

Popular aphorisms encourage us to “carpe diem,” “YOLO” or “live for the moment.” And on a fundamental level, that message has merit. Life is unpredictable, and it’s important to enjoy it. However, the idea also can be used to justify impulsive spending, allowing our present selves to win out over our future selves.

Consider a simple example: Spending $200 on a new pair of boots now may not seem like a major decision. However, if that same amount were invested and allowed to grow for decades, it could be worth thousands of dollars in the future.

This doesn’t mean you should never buy those boots—especially if you can afford them. The key is considering the trade-off and making that decision consciously.

Interestingly, carpe diem—often translated as “seize the day”—may have originally carried a more nuanced meaning. Some scholars suggest it would be better translated as “pluck the day,” an allusion to picking fruit or flowers at harvest time. Seen this way, the phrase originally may be more about appreciation and enjoying opportunities when the moment is right, rather than an exhortation to take impulsive action. That, perhaps, is a useful way to think about spending as well.

A PLAN THAT MAKES ROOM FOR LIVING

It might be easy to think that financial advice is all about pushing you to cut back and save more. In reality, it’s about finding balance. Together, we can build spending strategies that reflect what matters to you most, so you can feel confident about your future without putting your present happiness on hold.

MARKET RETURNS DURING PAST GEOPOLITICAL CONFLICTS

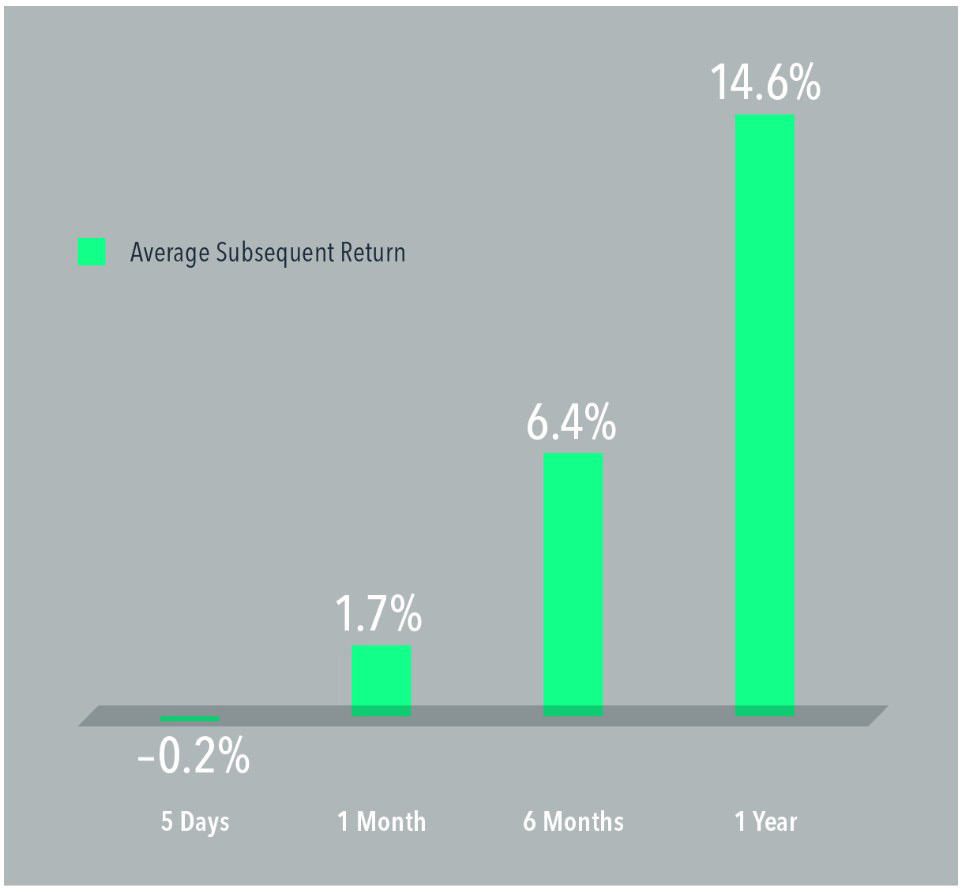

We noted in a recent piece that geopolitical conflicts don’t have to result in disappointing subsequent stock returns because markets are forward-looking and set prices for positive expected returns. But how have markets actually fared during previous geopolitical incidents? Based on 36 years of history, the answer has largely been good news.

While the classification of an event as a geopolitical conflict is subjective, we identified 21 global events since 1990. Charting returns starting from the onset of these events, we see slightly negative returns on average for the first five days, but then positive average returns over subsequent horizons. This would seem consistent with a market resetting prices in light of negative news at the start, which then sets up a positive expected return in the absence of further disappointing developments. After one year, the average return was 14.6%. By comparison, the average return across all rolling 12-month periods was 12.4%.

This is not to imply we’re “out of the woods” when it comes to a market downturn. The 12-month market return was negative for two of the 21 events. There’s always the possibility for worse-than-expected developments, which might provoke further negative reaction from markets. But the takeaway from these data is that investors shouldn’t shy away from stocks during a period of global conflict.

Exhibit 1

Average US Stock Market Returns Following Major Geopolitical Events

1990-2025

Article By: Wes Crill, PhD

Senior Client Solutions Director and Vice President at Dimensional Fund Advisors

See below for disclosures.

THE LEGACY CONTINUES

Again, as usual many made their annual voyage to Omaha, Nebraska for this year’s annual meeting for Berkshire Hathaway which was held on May 2nd, 2026 to see what changes, if any, might be taking place or are on the horizon. This was the first year that Warren Buffett was not the CEO of Berkshire Hathaway, and this year’s annual shareholders’ meeting was conducted by Greg Abel, Warren Buffett’s hand-picked successor. The theme of this year’s meeting was “the legacy continues” which was evident from what Greg Abel explained about how the company was to be run under his leadership. It did not take long to surmise that Greg Abel is very knowledgeable and plans to do things by the “manual” developed by Warren Buffett on how to run the business. Even though Warren Buffett is no longer the CEO of Berkshire Hathaway, he is the Chairman of the Board and goes to the office 5 days per week to render his advice and help in an advisory capacity.

Warren was present for the shareholders’ meeting (sitting with the other Board members) and spoke on a couple of occasions. During his talks, he stressed that investing should be treated as “investing” not “gambling”. Investing is for the long-term—not a way to turn a quick buck. He also talked about his management style which was to abide by the “Golden Rule”—treating others the way that you want to be treated yourself. “Integrity” was stressed at the meeting by Greg Abel as to how the company will be run in the future.

To begin the question-and-answer period, an AI-created deepfake of Warren Buffett was used to ask a question about how a person like him, being 95 years old, should look at investing. This situation was shown for everyone to see how careful you must be with the use of AI, and how you need to question if you are dealing with reality or if it is “fake”. The deepfake appeared to be very real to show how you can be easily fooled. AI can be a very helpful tool, but must be carefully scrutinized.

Market Returns During Past Geopolitical Conflicts disclosures:

Past performance is not a guarantee of future results. Actual investment returns may be lower. In USD. US Market is represented by the Fama/French Total US Market Research Index. The Fama/French indices represent academic concepts that may be used in portfolio construction and are not available for direct investment or for use as a benchmark. See “Index Descriptions” for descriptions of the Fama/French index data. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. The chart is for illustrative purposes only and is not indicative of any investment. The sample includes 21 geopolitical events. Geopolitical events and their start dates include: Gulf War, August 2, 1990; Asian currency crisis, July 2, 1997; 1998 Iraq disarmament crisis, February 18, 1998; Russian Financial Crisis, August 17, 1998; Kosovo bombings, March 24, 1999; 9/11—terrorist attacks on the United States, September 11, 2001; Iraq War, March 20, 2003; Madrid bombings, March 11, 2004; London bombings, July 7, 2005; Iran nuclear tensions, July 31, 2006; Eurozone debt crisis, December 8, 2009; Arab Spring (Egypt), January 25, 2011; Libya intervention, March 19, 2011; 2014 Ukraine conflict, February 20, 2014; intervention in Syria, September 22, 2014; Paris attacks, November 13, 2015; Brexit vote, June 23, 2016; air strike on Syrian air base, April 7, 2017; North Korea nuclear test, September 3, 2017; Russia invades Ukraine, February 21, 2022; Israel-Hamas conflict, October 7, 2023. Events are selected to include major armed conflicts and notable upheavals and are not inclusive of all possible market events.

Expected return: An estimate of average anticipated returns informed by historical data.

Fama/French Total US Market Research Index: July 1926–present: Fama/French Total US Market Research Factor + One-Month US Treasury Bills.

Results shown during periods prior to each index’s inception date do not represent actual returns of the respective index. Other periods selected may have different results, including losses. Backtested index performance is hypothetical and is provided for informational purposes only to indicate historical performance had the index been calculated over the relevant time periods. Backtested performance results assume the reinvestment of dividends and capital gains. Eugene Fama and Ken French are members of the Board of Directors of the general partner of, and provide consulting services to, Dimensional Fund Advisors LP. The information in this material is intended for the recipient’s background information and use only. It is provided in good faith and without any warranty or representation as to accuracy or completeness. Information and opinions presented in this material have been obtained or derived from sources believed by Dimensional to be reliable, and Dimensional has reasonable grounds to believe that all factual information herein is true as at the date of this material. It does not constitute investment advice, a recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. Before acting on any information in this document, you should consider whether it is appropriate for your particular circumstances and, if appropriate, seek professional advice. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorized reproduction or transmission of this material is strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein. This material is not directed at any person in any jurisdiction where the availability of this material is prohibited or would subject Dimensional or its products or services to any registration, licensing, or other such legal requirements within the jurisdiction.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd., Dimensional Japan Ltd., and Dimensional Hong Kong Limited.

RISKS – Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

UNITED STATES – Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

Investment products: • Not FDIC Insured • Not Bank Guaranteed • May Lose Value

Dimensional Fund Advisors does not have any bank affiliates.

Investments provided through McMill Wealth Inc, a Nebraska Corporation, Registered Investment Advisor

This material is derived from sources believed to be reliable, but its accuracy and the opinions based thereon are not assured.

The articles and opinions in this publication are for general information only and are not intended to serve as specific financial, accounting or tax advice