HOW CAN I GIVE MY KIDS A HEAD START ON INVESTING?

The earlier you start investing, the better. You’ve heard this advice before, and hopefully it’s helped you make some smart financial moves. But there’s one group that may not yet know this bit of investing wisdom: the kids in your life. Whether you have kids, grandkids, or nieces and nephews, these youngsters have an enormous asset on their side: time. Helping them get an early start with investing can give them a huge financial boost. The good news is that there are a lot of ways you can help set up the next generation for financial success. Let’s explore some options.

529 PLANS: A GREAT TOOL FOR FUTURE EDUCATION COSTS

With rising education costs, 529 plans are often the first type of investment account that parents open for their children. It makes sense. They’re one of the best tools available for long-term education savings.

You probably already know the main benefits: tax-deferred investment growth, tax-free withdrawals for qualified education expenses and no federal contribution limits (though gift tax may apply beyond annual contributions of $19,000 for 2025). Friends and family can contribute, and funds can be used for a growing range of expenses: college, of course, but also up to $10,000 per year for K–12 tuition. And excess funds can be rolled over to another family member, used to pay for grad school or even used to pay off student loans.

CUSTODIAL ACCOUNTS: MORE FLEXIBILITY BUT LESS CONTROL

But what if you want to help your child invest toward future expenses not covered by a 529 plan, like car repairs, travel or the down payment on a house? That’s where custodial accounts might be appropriate. UGMA (Uniform Gifts to Minors Act) and UTMA (Uniform Transfers to Minors Act) accounts are typically easier to set up than a trust and can accomplish some of the same goals.

Custodial accounts let you invest in a variety of assets in a child’s name, including stocks, bonds, mutual funds and even real estate. UTMA accounts also let you hold complex assets like art and intellectual property. There are no contribution limits, and the funds can be used for anything that benefits the child while they’re still a minor. However, your child takes complete control over the account when they reach adulthood (usually age 18–21, depending on the state). At that point, they can use the funds for any purpose. Note that investment earnings may be subject to the so-called kiddie tax. For 2025, that means the first $1,350 of unearned income is tax-free, the next $1,350 is taxed at the child’s marginal rate, and anything above that may be taxed at the parent’s marginal tax rate. Another word of caution: Custodial accounts are considered the child’s asset, which may impact financial aid eligibility more than a 529 plan would.

ROTH IRAS: EVEN KIDS CAN START SAVING FOR RETIREMENT

If you’re thinking even longer-term, you can help your kids start saving for retirement by opening a custodial Roth IRA on their behalf. Roth IRAs allow them to enjoy decades of tax-free investment growth and tax-free withdrawals in retirement.

To fund any IRA, the child must have earned income—such as from babysitting gigs or slinging ice cream over the summer. Those contributions cannot exceed their total earnings or the $7,000 annual limit (for 2025), whichever is lower. Then, once the child reaches adulthood (usually 18–21, depending on the state), they can transfer those savings to a new account to keep building a bright financial future.

BEYOND INVESTMENT BENEFITS: TEACHING FINANCIAL LITERACY

One of the best financial gifts you can give a child isn’t just money—it’s knowledge. And opening an investment account is an opportunity to introduce your family to some of the most important concepts in personal finance. You can start by talking to your kids about budgeting, saving and what it means to invest. Review account statements with them to highlight the power of compounding and the benefits of tax deferral. Use the target-date portfolios in a 529 plan to teach your kids about the value of diversification. And bring them into decisions when picking investments for a custodial account or Roth IRA. It’s a great chance to discuss the long-term advantages of choosing broader market exposure over trying to pick single stocks.

The earlier a child understands how money and investing works, the better their odds for achieving long-term financial goals. We’re here to help you give them that head start—whether it’s setting up accounts, discussing financial strategies or sharing more ideas for teaching kids about money.

LONGER HORIZONS LOOK BETTER FOR STOCKS

For many investors, it’s hard not to follow the daily fluctuations of the stock market. But day-to-day volatility is a reminder that stocks are best considered a long-term investment.

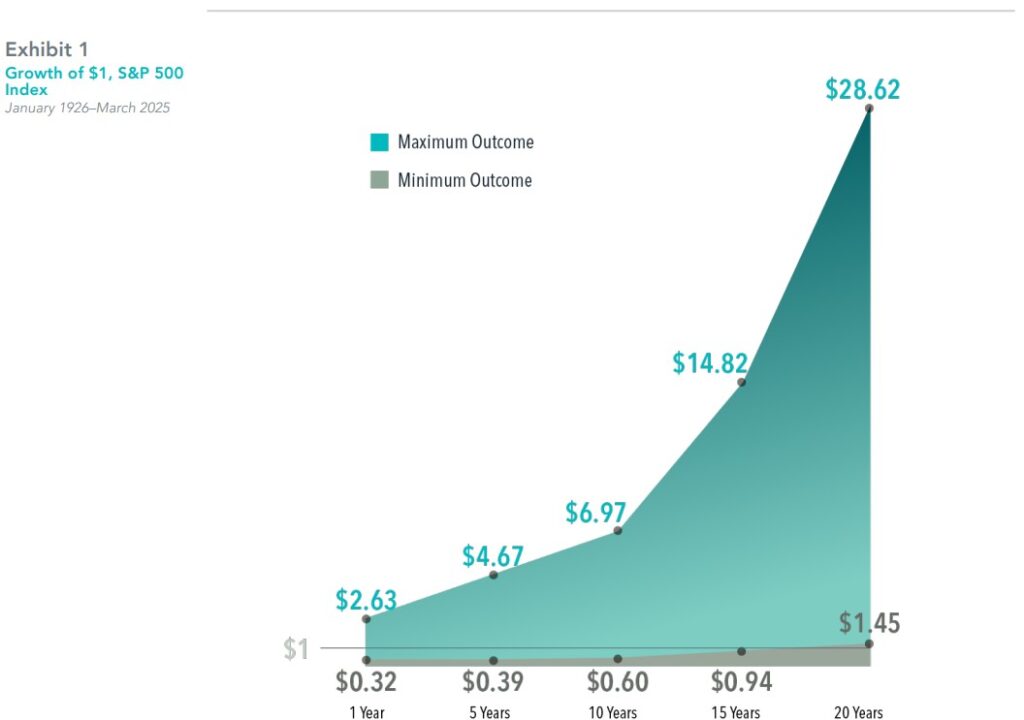

Part of the reason stocks have higher expected returns than bonds is uncertainty over shorter horizons. For example, the S&P 500 Index return was negative in about 24% of overlapping one-year periods from January 1926 through March 2025. The worst outcome over these one-year periods was about –68%, dropping $1 in invested capital to just $0.32.

Things have looked better over longer horizons, with the caveat that the number of independent observations among rolling return windows dwindles as the horizon lengthens—just five for the 20-year returns. But the frequency of negative returns decreases as the investment period expands, and no stretch over 184 months has been negative.

This is not to imply stocks are less risky in the long run. The range between best and worst outcomes becomes vast at the longer time horizons. But the data we have suggest the likelihood of losing money in stocks is far lower if they are viewed as long-term investments.

Of course, most investors also have short-term needs for their capital. That’s why most of us have a mix of stocks plus risk-management assets, such as bonds. A thoughtfully designed asset allocation helps balance short-term liabilities with long-term growth of wealth. And that’s a recipe for staying disciplined and paying less attention to the throes of stocks each day.

Past performance is no guarantee of future results.

Growth of $1 computed over rolling monthly periods for the S&P 500 Index assumes reinvestment of income and no transaction costs or taxes. Outcomes are reported for the minimum and maximum of these observations. There are 1,180 overlapping one-year periods, 1,132 overlapping five-year periods, 1,072 overlapping 10-year periods, 1,012 overlapping 15-year periods, and 952 overlapping 20-year periods. The analysis is for illustrative purposes only and is not indicative of any investment. S&P data © 2025 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Indices are not available for direct investment.

This article originally appeared in Above the Fray, a weekly newsletter for Dimensional clients.

Please see end of this post for important disclosures.

IS GOLD A SAFE HAVEN?

Not since the release of the third Austin Powers movie have I heard so much talk about gold. Stellar recent returns account for some of that — gold was up 25% year-to-date as of April 30. But another reason is the belief among some market participants that gold represents a safe haven, an asset to stabilize the portfolio when equity markets are choppy.

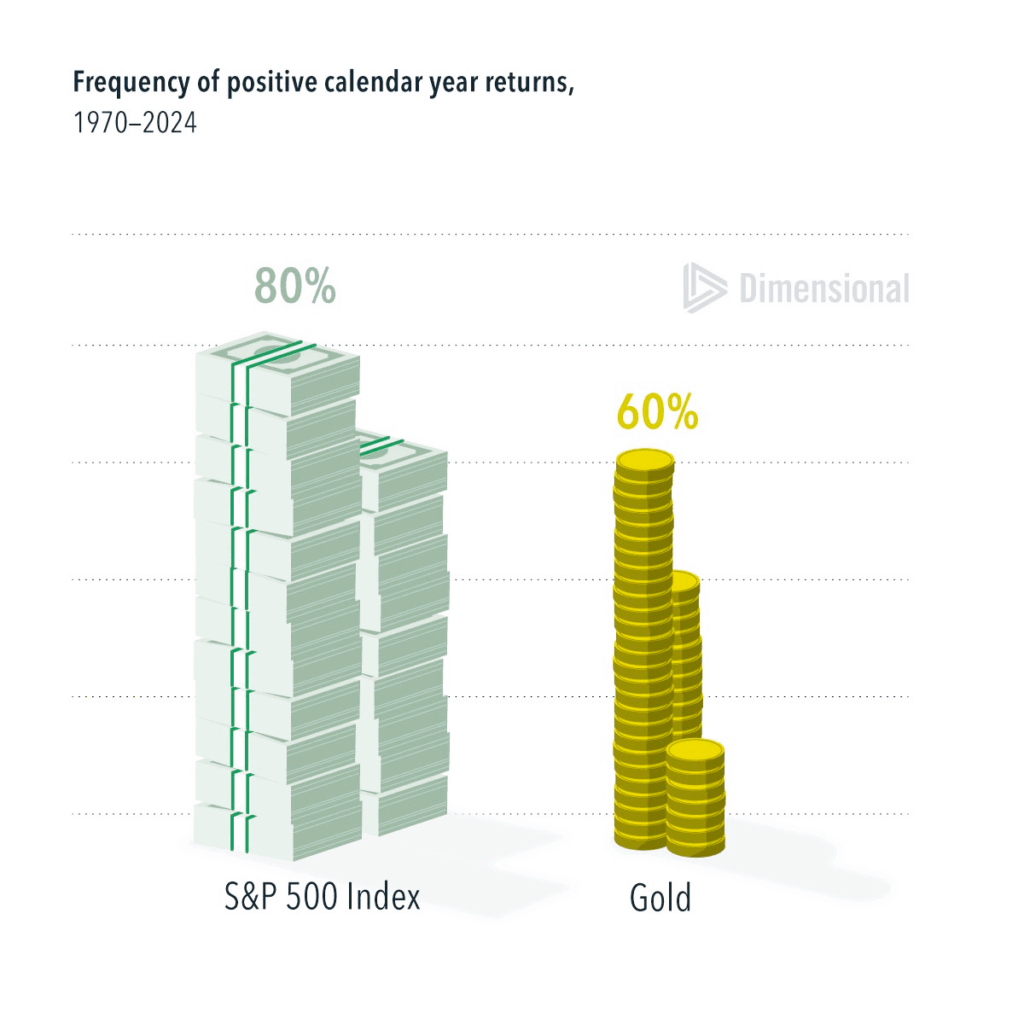

The problem with that story is gold has been far from immune to drawdowns. In fact, since 1970,

gold has been positive in just 60% of calendar years while the S&P 500 Index has been positive in 80%.

Investors hoping for a safe haven may not find it with gold.

Past performance is not a guarantee of future results.

In USD. S&P data © 2025 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Gold source: Bloomberg returns from composite prices. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Please see end of this post for important disclosures.

THE END OF AN ERA AND BEGINNING OF A NEW CHAPTER

Many made their annual voyage to Omaha, Nebraska for this year’s annual meeting for Berkshire Hathaway, which was held on May 3rd, 2025, to see and hear “the Oracle of Omaha” – Warren Buffett. This meeting marked an end of an era with Warren Buffett announcing that he would be stepping down at the end of 2025 as CEO of the company. He announced his recommendation of Greg Abel, Vice -Chairman of Non-Insurance Operations to succeed him as CEO of the company as of January 1, 2026. Buffett will remain as Chairman of the Board. The usual crowd-size for this event is somewhere around 40,000+ with people coming from around the world with many from China, again this year. Warren Buffett, who is 94 years old, ended the meeting after making his announcement of stepping down. With that, the crowd roared with applause, and rose to their feet to give Buffett a standing ovation. He laughingly responded by saying that their response to his announcement could be taken two ways.

It was also noteworthy this year that 2025 marked the 60th anniversary of Berkshire Hathaway which started in 1965. Honesty and integrity were virtues that Buffett tried to abide by in his management style of the company.

Many were there to latch on to some tidbit of information that they hoped could make them an automatic, overnight success at investing. Some were there to have just one more occasion to tap the knowledge and philosophies of Warren Buffett. His message is usually the same. That is, to not be easily influenced by the media when making investment decisions – stay rational. They often say that it is not how smart you are, but how able you are to control your emotional behavior that will determine how successful you are in investing. In responding to questions, he made several references to what Charlie Munger’s view might have been on many specific questions.

Volatility and uncertainty in the market seems to always be present, and no one knows what the future will hold. This is definitely true this year with all of the tariff negotiations that have been going on recently.

There is no way to predict how volatile the market will be in the future, but we are here to help when controlling your emotional behavior may not be an easy task. Contact us with your questions and any concerns, and enjoy your summer!

Disclosures for Longer Horizons Look Better for Stocks:

dimensional.com

Written By: Wes Crill, PhD, Senior Client Solutions Director and Vice President | Dimensional Fund Advisors – April 29, 2025

The information in this material is intended for the recipient’s background information and use only. It is provided in good faith and without any warranty or representation as to accuracy or completeness. Information and opinions presented in this material have been obtained or derived from sources believed by Dimensional to be reliable, and Dimensional has reasonable grounds to believe that all factual information herein is true as at the date of this material. It does not constitute investment advice, a recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. Before acting on any information in this document, you should consider whether it is appropriate for your particular circumstances and, if appropriate, seek professional advice. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorized reproduction or transmission of this material is strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

This material is not directed at any person in any jurisdiction where the availability of this material is prohibited or would subject Dimensional or its products or services to any registration, licensing, or other such legal requirements within the jurisdiction.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are

Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd., Dimensional Japan Ltd., and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

RISKS

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

UNITED STATES

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

Investment products: • Not FDIC Insured • Not Bank Guaranteed • May Lose Value

Dimensional Fund Advisors does not have any bank affiliates.

Disclosures for Is Gold a Safe Haven?:

dimensional.com

Written By: Wes Crill, PhD, Senior Client Solutions Director and Vice President | Dimensional Fund Advisors

Disclosures: All expressions of opinion are subject to change. This information is not meant to constitute investment advice, a recommendation of any securities product or investment strategy (including account type), or an offer of any services or products for sale, nor is it intended to provide a sufficient basis on which to make an investment decision. Investors should consult with a financial professional regarding their individual circumstances before making investment decisions. Diversification neither assures a profit nor guarantees against loss in a declining market.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

Investment products: • Not FDIC Insured • Not Bank Guaranteed • May Lose Value

Dimensional Fund Advisors does not have any bank affiliates.

Investments provided through McMill Wealth Inc, a Nebraska Corporation, Registered Investment Advisor

This material is derived from sources believed to be reliable, but its accuracy and the opinions based thereon are not assured.

The articles and opinions in this publication are for general information only and are not intended to serve as specific financial, accounting or tax advice