EDUCATING THE NEXT GENERATION ABOUT FAMILY WEALTH MANAGEMENT

Over the next few decades, an enormous amount of wealth is expected to pass from older to younger generations. This has been dubbed the “Great Wealth Transfer,” and one estimate suggests that $124 trillion will change hands by 2048. It’s an eye-popping figure, to be sure, but it also highlights the reality that many families are, or soon will be, navigating how to pass on their wealth. A top-of-mind question: Is the next generation ready to take on the responsibility?

Wealth is not just cash in the bank; it can include investments, real estate, businesses and more that require stewardship and foresight. Successful management means preserving and growing assets and using them wisely. Striking the right balance here is key: For the next generation to succeed, it takes intentional preparation and education.

PLANT THE SEEDS OF FINANCIAL LITERACY

Where to begin? In an ideal world, financial education starts in early childhood and is treated as an open and ongoing conversation as kids age. The goal is to build financial literacy gradually, so wealth management feels natural rather than overwhelming.

When kids are young, this might mean introducing simple topics like the difference between saving and spending. Managing an allowance can help put those ideas into practice. As kids get older you can begin introducing more complex topics, such as investing, compound interest, debt and taxes.

It’s equally important to engage adult children, many of whom may have received no other formal financial education. While 29 states now have K–12 financial education requirements in public schools, this focus has largely come to the forefront only in the last few years. If your kids are adults now, they may have missed out. So it’s worth finding out what they know, what they don’t know and what they’d like to know more about.

PUT STRUCTURE AROUND LEARNING

In addition to ongoing conversations about money, your family might benefit from more intentional ways of building financial literacy. Some families hold regular financial meetings where they share goals, key issues and address questions or concerns. Others put together more formal workshops with wealth advisors or other experts. There also is a wealth of credible educational content online that is built to both educate and engage audiences around financial literacy topics.

TURN CONVERSATIONS INTO ACTION

Eventually, theory should give way to practice. As younger family members learn the basics, you might consider providing a “practice portfolio,” giving them the chance to make investment decisions with small amounts of money and learn from their successes and mistakes. When family members have honed their knowledge, consider assigning them real responsibilities that match their skills and interest. This might mean relatively simple tasks like helping guide gifts made through a donor-advised fund. Or these responsibilities could be more involved, such as taking a role in the family business or helping to make investment decisions with the family’s wealth.

With your guidance and oversight, these experiences can help develop confidence and capability.

GROUND WEALTH IN PURPOSE AND VALUES

One of the most important things that helps guide families on how to grow and spend wealth is imparting a strong value system. Values can help you frame wealth as a tool rather than a goal.

Your values will be unique to you, but some worth considering may be:

• Stewardship: Recognizing the responsibility that comes with wealth. Stewardship encourages careful management and intentional choices so resources can benefit both current and future generations.

• Giving back: Using wealth to help create positive change in your community and the greater world.

• Self-worth beyond wealth: Remembering that wealth is a tool to achieve goals—whether gaining an education, pursuing passion or giving back, for instance—not a measure of personal value.

By grounding financial decisions in values, families can help prevent counterproductive or reckless financial decisions, foster responsibility and ensure wealth is not seen as something to be simply consumed.

KEEP THE CONVERSATION GOING

Discussing money isn’t always easy, and for many families, it’s downright taboo. While 66% of Americans say conversations about wealth are important, 62% say they never have them.3 But getting over this hurdle is incredibly valuable. The most successful families treat wealth education not as a one-time event, but as an ongoing process that evolves as your family grows and your financial picture changes. We can work with you to create an environment where family members can openly discuss the unique challenges and opportunities that come with wealth.

HAVE YOU RECEIVED A LETTER FROM THE SSA ABOUT “POTENTIAL PRIVATE RETIREMENT BENEFITS”?

TIMING AND PURPOSE OF LETTER

Each year—typically between August and October—the Social Security Administration (SSA) mails notices to individuals who may have unclaimed 401(k), pension, or other retirement benefits from a previous employer.

If you recently received one of these letters, don’t ignore it!

It could mean there’s a retirement account in your name waiting to be claimed.

HOW TO PROCEED WITH LETTER

Contact us and we would be happy to help you:

• Identify which employer and plan the notice refers to

• Locate and recover any old 401(k) or pension benefits

• Consolidate those assets into a Rollover IRA for easier management and continued growth

The letter usually comes from the Social Security Administration and includes a “Plan Number” and employer name. You will want to keep the letter handy when you reach out for guidance.

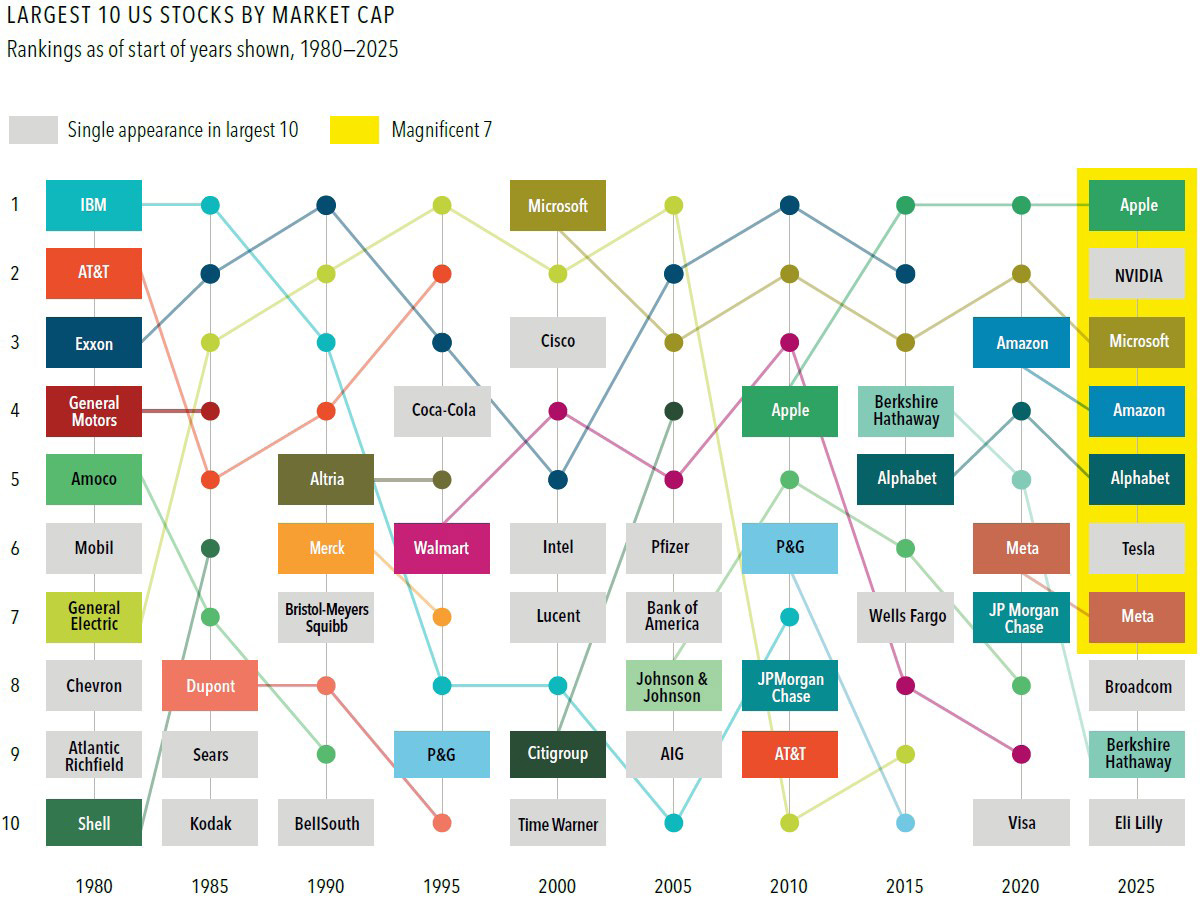

WILL THE MAGNIFICENT 7 STAY ON TOP?

The Magnificent 7 entered 2025 among the Top 10 largest US stocks. But before making an outsize bet on gains from these technology giants, investors should consider a few lessons from market history.

It’s hard to stay on top. For example, only three of the ten biggest companies from 1980 made the 2000 list—and none of them was in 2025’s Top 10.

Industries ebb and flow. Technology-focused firms currently dominate the list. But in 1980, six of the ten largest companies were in the energy sector.

New technology doesn’t benefit only tech firms. Throughout history, companies across industries have used technology to innovate and grow.

Diversification enables investors to share in the success of today’s top companies while staying positioned to benefit from tomorrow’s market leaders.

Past performance is not a guarantee of future results.

Investing risks include loss of principal and fluctuating value. There is no guarantee an investment strategy will be successful.

The Magnificent 7 stocks are Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla.

This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. Named securities may be held in accounts managed by Dimensional.

Source: Dimensional, using data from the Center for Research in Security Prices and Compustat. Includes all US common stocks. Largest stocks identified at the end of the calendar year preceding the respective period

by sorting eligible US stocks on market capitalization using data provided by the CRSP, University of Chicago.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

Investment products: • Not FDIC Insured • Not Bank Guaranteed • May Lose Value

Dimensional Fund Advisors does not have any bank affiliates.

PREDICTIONS

I recently read an article about predictions for our area for the upcoming winter.

In the article the author took a look at predictions made by the Farmers Almanac,

the Old Farmers Almanac, the Weather Service, the old wives-tales about ground

fog and the woolly worm whether it was fat or slim. Some of the various means

of predicting how the winter would go did coincide at least partially, but most of

them were quite different. In hindsight, when the winter is over is truly the only

way we will know for sure the outcome.

It is very similar with the markets. Everyone seems to have a different viewpoint

on how the markets will trend in the future. Even those with Nobel Prizes in

Economics will admit that they can not accurately predict the markets with any

consistency. The future is unknown until it turns into the present.

Not accounting for life-changing events, we have attempted to build a portfolio

that would fulfill your needs for the long-term based upon your risk aversion and

plans for your future. By focusing on your long-term plan, you shouldn’t need

to worry about what is going on daily in the market. You have a portfolio that is

diversified and based upon your wants and desires.

We are often asked “when would be a good time to invest?” No one actually

knows with any certainty the optimal time to invest. However, we usually say

that anytime is probably the right time to invest. The market will fluctuate

both higher and lower over time, and we can help you take advantage of those

fluctuations through rebalancing the investments within your investment

portfolio. Rebalancing provides the basis for selling “high” and buying “low”

during fluctuations in the market. We use this formula for a successful investment

experience over the long term.

So no matter what goes on in the market on a daily basis during 2026, don’t

worry about it. Your portfolio was designed specifically for you to be able to stick

with your financial plan. However, if you do experience a life-changing event,

please consult with us. We will be glad to help you determine if any adjustments

to your financial plan and investment portfolio need to be made under those

circumstances.

Remember to thank veterans and first-responders that you know for the many

sacrifices that they have made to make our country safe and free, and recognize all

of the blessings that we have enjoyed in 2025. We are very fortunate and thankful

to have had the opportunity to serve you as our clients in the past year and look

forward to continue our professional relationship with you in 2026.

Best wishes to you and yours to have a joyous holiday season, and a happy,

healthy, and prosperous new year!

Investments provided through McMill Wealth Inc, a Nebraska Corporation, Registered Investment Advisor

This material is derived from sources believed to be reliable, but its accuracy and the opinions based thereon are not assured.

The articles and opinions in this publication are for general information only and are not intended to serve as specific financial, accounting or tax advice