Investment Philosophy

We believe in Modern Portfolio Theory and have access to high-quality institutional investment firms with a unique implementation of this theory into an entire diversified family of mutual funds. Each fund captures the return behavior of an entire asset class, letting us accurately diversify clients’ investments across multiple asset classes-precisely incorporating the level of risk with which each investor is comfortable. Asset class investing is a systematic, global allocation of your portfolio.

Passive Asset Class Management Approach

As you familiarize yourself with McMill Wealth, you will quickly notice our strong focus on implementing this passive asset class management approach as the best investment strategy. Other advantages of this approach include:

- Lower costs – Passive asset class funds traditionally have lower operating expenses and transaction costs (and thus higher expected returns) than do comparable actively managed funds;

- Lower portfolio turnover – Our turnover is roughly 12%, while the industry average is almost 70%;

- Greater tax efficiency – Passive asset class funds have relatively low turnover, so less of your annual return is consumed by taxes;

- Broad diversification/risk reduction – Our typical portfolio may include over 14,000 stocks, while the industry average is around 2,000 stocks;

- Long-term perspective – No HOT money, which is money that moves in and out of investments frequently. We manage wealth with a long-term perspective in mind.

- Control of asset allocation – Concentrating on staying diversified captures 94% of the results;

- Passive asset class funds – Capture separate dimensions of worldwide returns;

- Academic research – Points to the importance of asset class selection, not market timing or security selection.

Importance of Passive Asset Class Investment Approach

(Being Broadly Diversified)

At McMill Wealth, we are strong advocates of the passive asset class investment approach. We are convinced that a passive investment approach, which emphasizes broad diversification and market returns in a controlled risk, low cost, tax efficient environment is the right answer for individuals as well as institutional investors.

The graph to the right demonstrates that asset class selection, not market timing or security selection, is the most important determinant of how well a portfolio performs.

Flaws of Market Timing

Market timing is the shifting of portfolio assets in and out of the market or between asset classes and involves actively buying and selling those stocks that are believed to be mispriced so to capitalize on price corrections. We believe that markets are efficient and quickly and accurately reflect available information so it would be very unlikely that a manager could find a mispriced stock. The flaws of market timing can be demonstrated by removing the effects of the best trading days in the market as shown below.

How could anyone predict when those few “best days” will occur?

| 1991-1998 | Returns* |

|---|---|

| 2,023 Trading Days | 19.87% |

| Minus 10 Best Days | 13.63% |

| Minus 20 Best Days | 9.21% |

| Minus 30 Best Days | 5.35% |

| Minus 40 Best Days | 1.90% |

Source: John D. Stowe, A Market Timing Myth. Journal of Investing, Winter 2000. Performance is historical and does not guarantee future results. Information from sources deemed reliable, but its accuracy cannot be guaranteed. *CRSP value-weighted index with dividends reinvested. Compound annual returns assume a 1% transaction cost per portfolio turnover.

Flaws of Stock Selection

Stock selection is the finding of “underpriced” companies or industries. It is best to demonstrate the inability to pick a winning stock combination by showing the following data from the Bogle Financial Center and Lipper, Inc., who studied the performance of 851 U.S. equity mutual funds for two consecutive four-year periods.

| Top Ten in: 1996-1999 | Same Funds in: 1999-2002 |

|---|---|

| 1 | 841 |

| 2 | 832 |

| 3 | 845 |

| 4 | 791 |

| 5 | 801 |

| 6 | 798 |

| 7 | 790 |

| 8 | 843 |

| 9 | 851 |

| 10 | 793 |

It is one thing to say that past performance is no guarantee of future results, but this data demonstrates that this year’s winners may be next year’s biggest losers. The chart above illustrates that the #1 annual return fund from 1996-1999 ended number 841st out of 851 total funds in the subsequent 4-year period. In fact the best ranking for the previous top ten funds was 790th.

This information drives home the fact that the most important way NOT to pick funds is to look at short-term (five years or less) performance.

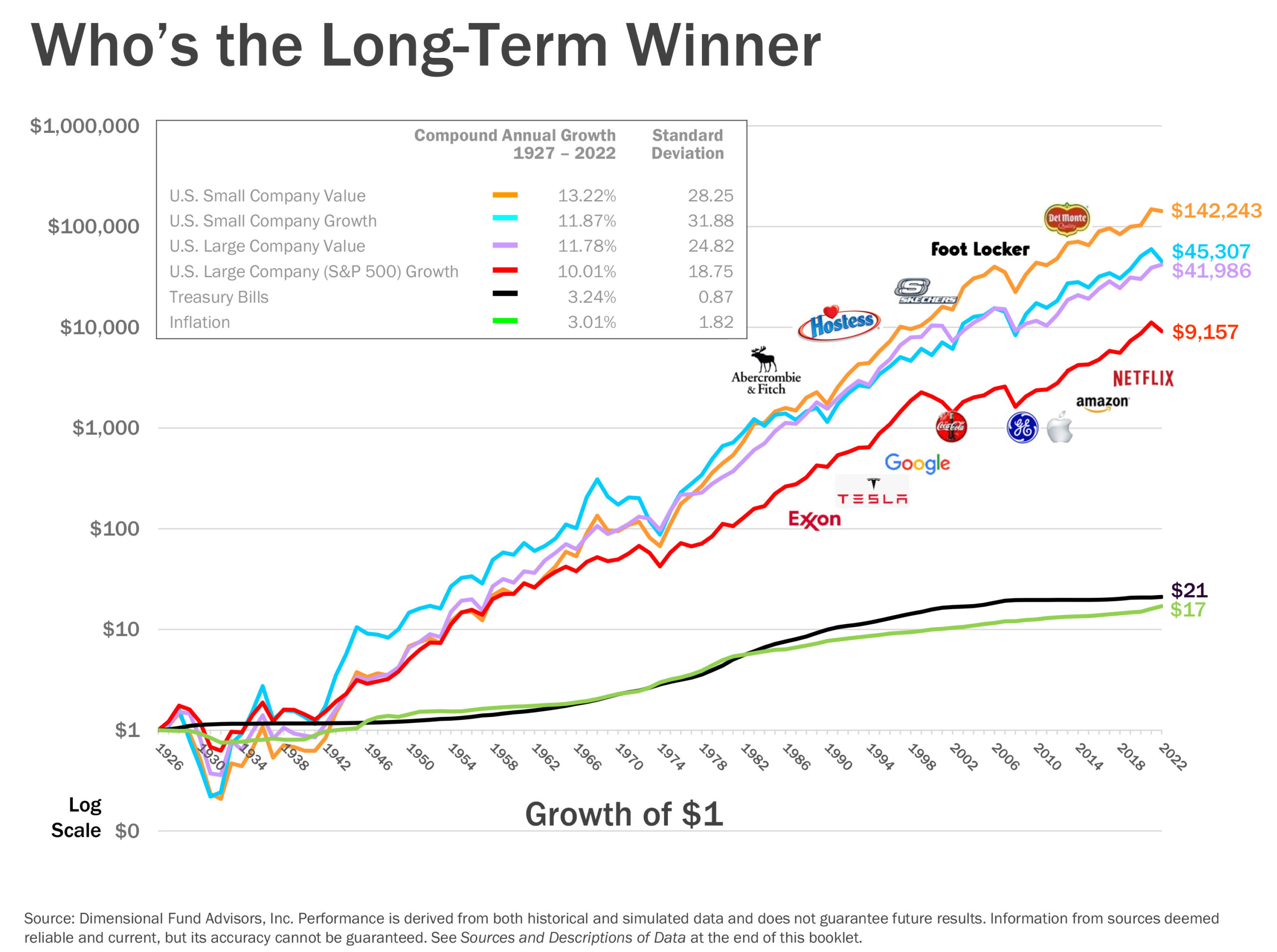

A Better Way to Pick Funds

The graph to the right illustrates returns of the distinct asset classes in showing the growth of $1. The optimum portfolio would capture a particular “dimension” of each of these broad asset classes within a globally-diversified portfolio.

Notice how holding bonds and CDs can be hazardous to your financial health due to inflation and taxes. You can also see that the growth of $1 for small cap value greatly exceeds the S&P 500 (large cap).

Diversify Across Asset Classes

Modern Portfolio Theory (MPT) is founded on the idea that for every level of risk there is an optimum portfolio strategy that results in the maximum return for that level of risk. To achieve this optimum risk/return portfolio, investors should diversify across asset classes. By following this diversification method, MPT holds that you not only reduce the risk in a portfolio, but also increase the return of the portfolio.

We have found that this approach is translated best by Dimensional Fund Advisors into an array of mutual funds, each of which is rigorously designed to capture a particular “dimension” of asset class within a globally-diversified portfolio. For more information about Dimensional, see our preferred funds.

To understand why McMill CPAs & Advisors allies itself with advisors who counsel this type of structured investment approach, click the related links below.